Understanding what influences your restaurant profit margin helps you assess the success of the business and make positive changes.

A slight improvement in your net profit makes a huge difference. It’s worth, therefore, investing in improving operations to boost your margin.

In this guide, we’ll examine the definitions and calculations for different types of restaurant profit margins and discuss the best ways to improve them through better inventory and purchasing management, tech integrations, and analytics.

What Is a Restaurant’s Profit Margin?

Your restaurant profit margin is the percentage of your revenue remaining after all expenses have been deducted. It can be calculated for each menu item or as an average for the whole business.

The restaurant profit margin takes into account all your revenue streams, from in-house dining and takeaway orders to branded merchandise and meal kits.

Your expenses include overheads like rent, staff salaries, and utility bills. They also include variable costs such as food costs, hourly staff wages, and equipment maintenance.

Let’s have a look at the two main types of restaurant profit margins.

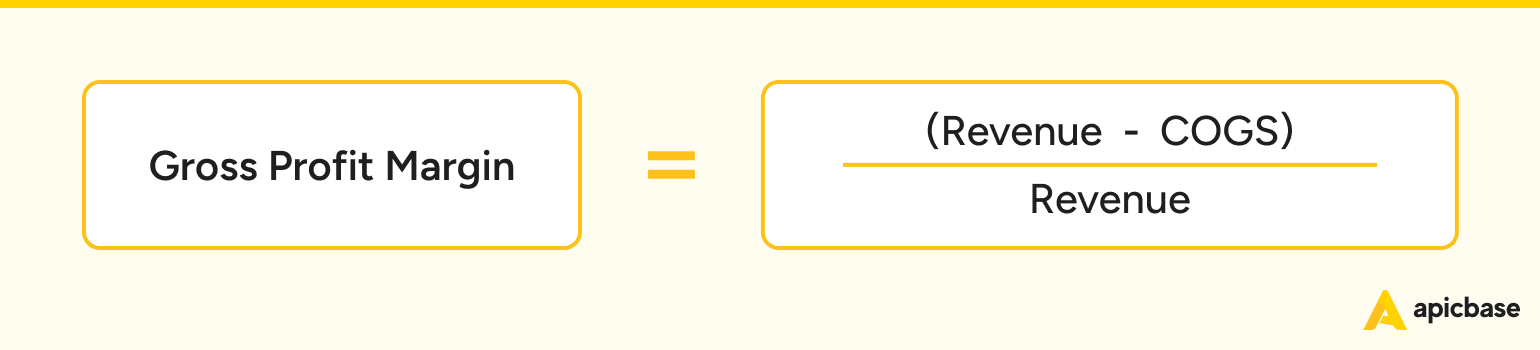

Gross profit margin

You calculate your gross profit margin by subtracting the cost of goods sold (COGS) from total revenue over a period. To calculate your restaurant’s COGS, you add up the cost of all the ingredients and packaging used to produce the items sold.

By only taking into account the cost of goods sold, the gross profit margin zeros in on your production costs. It tells you how efficient or wasteful your operations are, helping you reduce waste and lower your food costs.

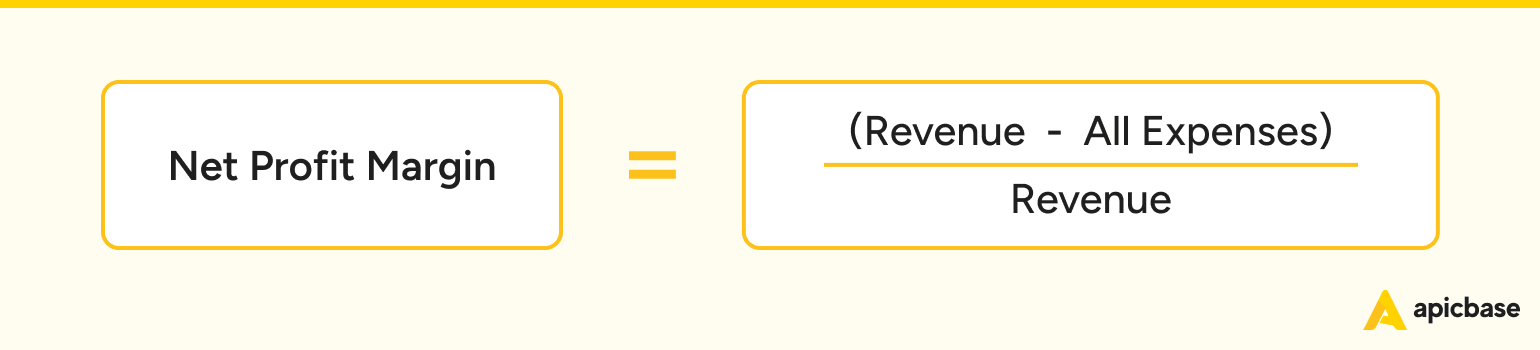

Net profit margin

Net profit is the difference between all operating expenses and total sales. It takes into account your COGS, overheads, and variable costs.

Because the net profit margin accounts for all operating expenses, it tells you whether your restaurant is making money on each dish sold and, therefore, whether it is profitable.

How to Calculate Your Restaurant’s Profit Margin

Using a simple formula, you can calculate your profit margin and know exactly how profitable your restaurant is. First, gather your sales numbers from your POS system and add up your monthly food costs and other expenses. Then, plug your numbers into the formulas below.

Gross Profit Margin Formula

Gross Profit Margin = (Revenue – COGS) / Revenue

Let’s say your revenue for April is €16,400, and your total COGS comes to €10,200.

Gross Profit Margin = (16,400 – 10,200) = 6,200

6,200 / 16,400 = 0.38

Your gross profit margin is 38%.

Net Profit Margin Formula

Net Profit Margin = (Revenue – All Expenses) / Revenue

Let’s say total expenses for the month are €11,100

16,400 – 14,300 = 2,100

2,100 / 16,400 = 0.13

Your net profit margin is 13%.

What’s the Average Restaurant Profit Margin

Restaurant profit margins vary widely depending on the establishment’s size, service style, and quality. According to public data, the average gross profit margin for US food service companies is 45%, while the average net profit margin is 7%.

For reference, our dashboards show that Apicbase users have an average gross profit of 73,3%, which is well above the industry averages. On a side note, we queried operations with over 20 units. The percentage reflects gross profit (revenue – COGS) on a corporate level. The profitability of individual units can be higher or lower.

There is no standard average net profit margin for restaurants. Profit margins typically range from 0% – 15%. However, we looked at the available online data, and most experts agree on the following average profit margins for restaurants:

Average margins by restaurant type and service model

- Full-service: Full-service restaurants are fully equipped with a team that includes managers, servers, chefs, bartenders, and hosts. They typically see profit margins of about 3% to 6%. These somewhat slim margins result from the hefty costs of keeping all those staff members on board and the expenses of maintaining the space. However, beverage sales offer a financial boost, yielding higher profits than food sales.

- QSR: Quick-service restaurants (QSRs), or fast-food restaurants, typically see profit margins between 6% and 11%. Compared to full-service restaurants, this higher profitability results from needing fewer staff members and lower product costs, making them more cost-effective to run.

- Catering: Catering businesses that operate without physical storefronts typically achieve profit margins in the range of 7% to 8%. While their product costs are similar to those of full-service restaurants, they benefit from having fewer staff members and eliminating the rent expense.

- Food truck: Food truck profit margins usually fall between 6% and 8%. While their ingredient expenses align closely with those of traditional sit-down restaurants, food trucks gain a financial edge by avoiding rent and having fewer utility costs.

Sadly, for many restaurants, this means a lot of hard work for not much of a reward.

When you’re spending thousands of euros a month on overheads, ingredients, and wages and only keeping 7%, or less, of all your revenue, you can see why many restaurants fail in their first few years.

However, there are ways to improve operations and maximise profit margins. Restaurants that put in the work may be able to achieve a healthier margin of up to 20%.

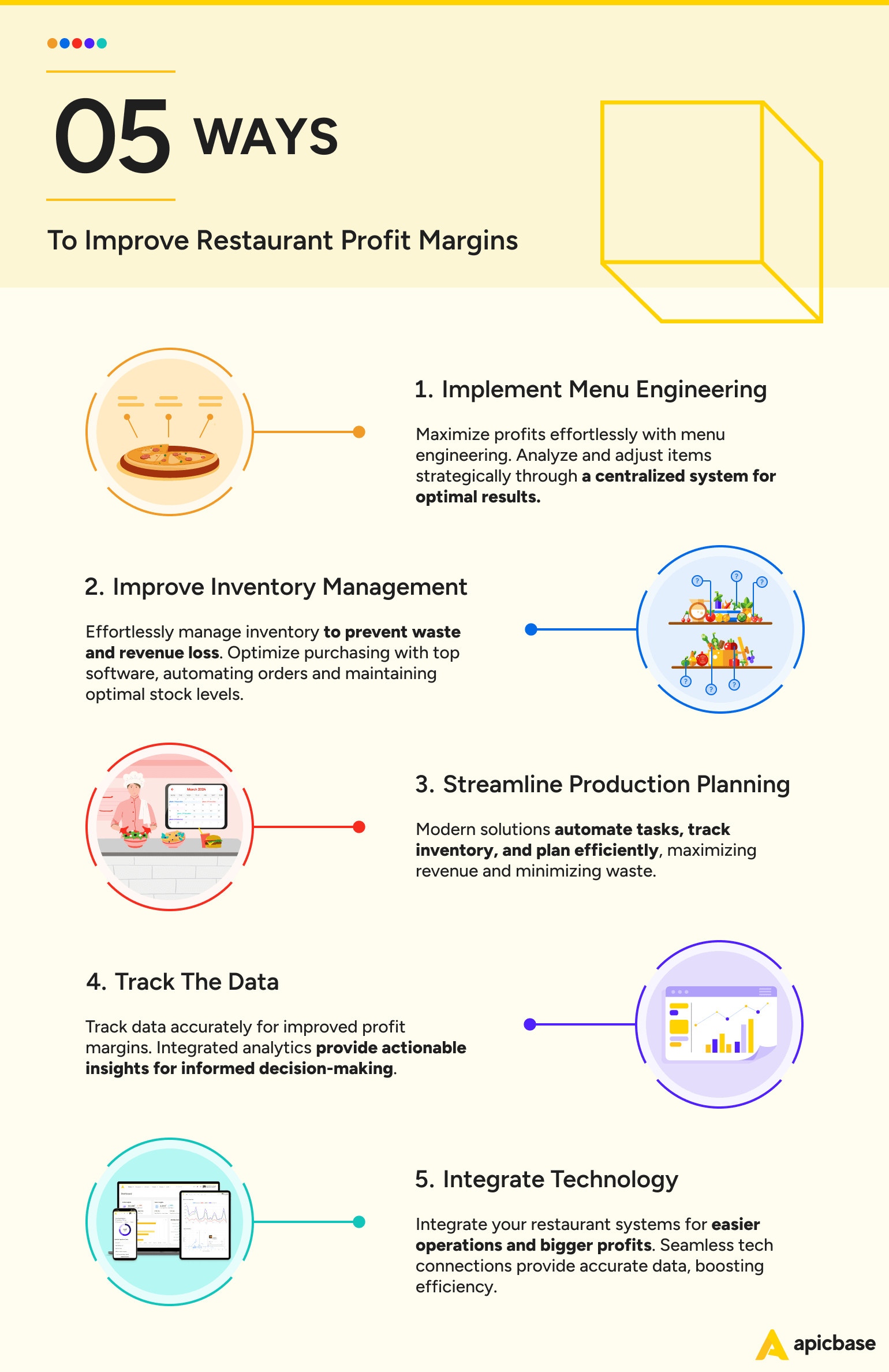

5 Ways to Improve Restaurant Profit Margins

Small tweaks and improvements to your operations can make a huge difference to profitability. If you increase your revenue slightly and cut a handful of unnecessary costs, your profit margin calculation dramatically improves.

Here are five ways to improve your operations and get a healthier profit margin.

1. Implement menu engineering

Menu engineering is the process of analysing the popularity and profitability of menu items and then making strategic changes to maximise profit margins.

Each menu item can be engineered for better profitability by making the right adjustments. Actions include improving supplier management, making production more efficient, reducing waste, improving yield, and optimising portion sizes.

A centralised recipe and menu management system makes it far easier to manage this complex process. It is your recipe data hub, from which you can:

- Get real-time menu costing data

- Develop profitable, popular menus for multiple brands

- Create allergen labels and nutritional scores

- Put menus into production using auto-generated prep lists and bills of materials

- Adjust portions, calculate yield, and reduce production waste and see the real-time effect on profitability.

2. Improve inventory management

Inventory management is about avoiding overstocking, which can lead to spoilage and waste, and understocking, which leads to empty shelves and missed revenue. To achieve the perfect balance, you’ll need to stay on top of stock levels and purchase orders and accurately predict demand.

The best inventory management software allows you to:

- Automatically turn bills of materials into purchase orders

- Set minimum stock levels so you never run the risk of empty shelves

- Create standardised order lists for regular purchases

- Set PAR levels and re-order automatically to keep stock at the optimum level

Taking control of your inventory and purchasing reduces waste and unnecessary spending and ensures you always have the ingredients you need to fulfil customer orders. Both of these factors are key to improving your profit margins.

3. Streamline production planning

Proper purchasing and production planning is a huge factor in controlling costs and remaining profitable. The latest procurement management solutions automate tasks and help you track inventory and plan production down to the smallest details.

When recipes and inventory data are stored in a single system, it’s easy to generate prep lists and production plans. Clear checklists ensure consistency across locations and production kitchens and ensure portions and food waste are under control.

Just like proper inventory management, a well-organised production system keeps costs under control, enables revenue to increase, and has a massive impact on your restaurant’s profit margin.

4. Track the data

Calculating profit margins regularly is crucial for improvement. To ensure actionable results, ensure you have complete and accurate data from all areas of the business.

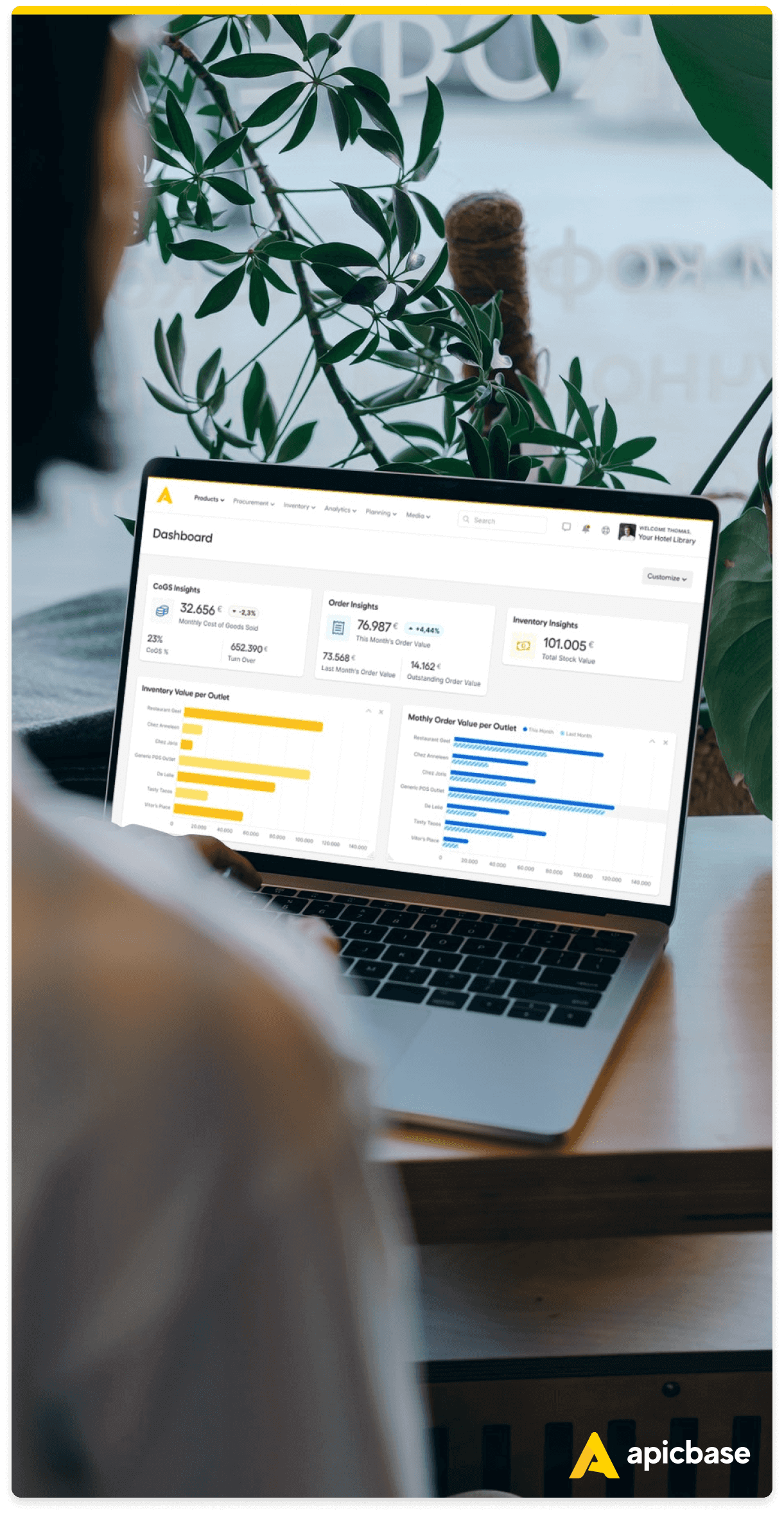

Restaurant analytics software keeps track of all your restaurant data in one place, giving you all the insights you need. Ideally, the analytics software should be at least integrated with your POS, recipe and inventory management software so you can be sure the data gives an accurate picture of your profitability.

5. Integrate technology

Linking your restaurant’s systems with your inventory management and analytics software simplifies tracking profit margins.

Payment processors and POS systems deal with the revenue coming into the business. Integrating the back-of-house and front-of-house systems gives you the accurate data you need to calculate and control your margins.

Integrations, either directly or through API, are a great way to create a seamless restaurant management ecosystem. Rather than your staff messing around with spreadsheets and multiple logins, they allow the team to manage operations from one system.

The more of your tech you can run from one system, the better. A unified platform for inventory management, analytics, and menu engineering gives you a foundation for operational success. And one that seamlessly integrates with your front of house tech gives you everything you need to achieve and maintain higher profit margins.

Supercharge Profits With Apicbase

Hospitality groups, restaurant franchises, and fast casual restaurant chains – across Europe and the rest of the world – trust Apicbase to reduce their operational costs and boost revenue potential.

Many of these restaurant companies use multiple central production kitchens on top of their regional restaurant locations, making operations extremely complex.

Apicbase streamlines your restaurant sites and makes operations less complex.

Large companies using Apicbase manage their inventory, purchasing, recipes, allergens, food costs and performance centrally in clear dashboards, not disjointed spreadsheets. There is an immediate benefit of 5% on average on food costs.

Get in touch to see how Apicbase could help your restaurant control costs and maximise profit margins.